How might we help people to achieve mental thriving through financial wellness?

You may hear the word "wellness" a lot in health care, but have you ever consider it been used in finance, like financial wellness?

Wellness is the state of not merely being free from calamity, but having a sense of flourishing. It's a descriptive outcome of one's current situation which can be easily influenced by the outside, like your financial state. So what are the motivations and limitations people have around financial planning? How can individuals more reliably cultivate a sense of financial wellbeing?

Over the course of our 14-week Introduction to Design Planning course in Spring 2019, our team developed 4 platforms to help people achieve financial wellbeing, as well to help Infosys and Allstate to identify potential business opportunities.

PHASE 1: PROJECT TIMELINE

This intense 14-week project can be roughly separated in 3 proportions: learning, designing and evaluating.

As our client determined to keep the topic loose, just gave us a general direction-healthcare&wellbeing. My team spent a few weeks to reframe the design challenge to one that felt interesting to the whole team while meaningful and had a potential business market to grow.

When participating in this project, the team had chances to practice design skills from the ID very owned "101 design methods". We fulfilled a whole design process from problem framing- research-insights framing-design opportunity identifying-design-evaluate. With productive client engagement and wonderful teamwork, we had chances to go beyond and had a memorable experience.

Design process is not linear.

PHASE 2: DESIGN CHALLENGE REFRAMING

"To be truly innovative, new problems and opportunities need to be thought through differently. Challenging conventional wisdom requires an understanding of how it came to be in the first place and thinking about how best to reframe it to be appropriate for a future possibility. Just as it is important to question prevailing conventions, it is equally important to question how innovation challenges are framed. "

——Vijay Kumar "101 Design Methods"

After brainstorming the client's topic-healthcare and wellbeing, we claimed that mental health occupies a space between wellness and healthcare.

As a culture, the United States lacks a shared understanding of mental health. It's not unusual for someone struggling to be described as going through a phase or to be scolded for a perceived lack of effort. Left untreated, mental health symptoms have an outsized impact on individuals and society.

One may ask for the causes, "financial status" as we found out was one of the main reasons that unstabilized our mental health condition. So as a team, we narrowed down to focus on how to keep people mentally thriving through finance approaches, and we used "value web" to help understand the value exchanges between the key entities in the play.

PHASE 3: SECONDARY RESEARCH BLITZ

Due to the considered timeline of this project, the team had limited time to get a sense of the problem scope. So we decided to focus on two directions, what & who.

What is happening in finance? Who are the next customers?

After quick rounds of research and sharing, we were able to piece together a robust view of the problem at hand. Moving forward, we developed a research tool based on learnings to help us with the primary research.

KEY LEARNINGS

What is happening in finance?

Customer perceptions of retail banks having a good reputation and being customer-driven are lower in 2019 than in 2009.

Most Americans aren't using financial advisors.

Just 21% have a financial advisor (outside of tax work) and just 27% have a written retirement plan.

64% of people with financial advisors feel unsatisfied about "having someone to talk to about money."

Who are the next customers?

Generation Z (those born after 1995) are different from Millennials (born 1980-1995). Where Millenials are idealistic, Generation Z grew up during the recession and is pragmatic.

Where Millennials focus on experiences, Generation Z teens tend to be more highly interested in saving money than millennials were at that age.

Where Millennials had helicopter parents, Generation Z is figuring it out on their own with less support and guidance.

"Almost half (47%) of Millennials report having received homework help from a parent compared to only 26% of Gen Z."

PHASE 4: PRIMARY RESEARCH

The research protocols involved two different interview guides for financial service users and industry subject matter experts. Additionally, we developed tools and activities to elicit richer information than might come out of traditional one-on-ones. This research addressed the following objectives:

-

Understand current & ideal financial situation

-

Understand how do people think their financial status relates to mental health

-

Understand what are the financial concerns that keep people out of bed

-

Understand how do people allocate their monthly income, and what can be viewed as emotional booster or drains

-

Understand ways that people use to help reduce financial stress

Elicitation Tools

After interviewing with 4 ID students, 1 ID faculty, 2 working adults, and 1 industry subject matter expert, we learned that:

-

High anxiety or low anxiety, it's always present

-

Lots of extremes, circumstance is either heaven or hell, no in-between exists

-

"Planning" feels too much like "predicting", since I'm bad at it, I don't want to do it at all

-

People preferred over digital tools

-

Mental health, it matters

PHASE 5: WORKSHOP & CLIENT ENGAGEMENT

How to communicate "THE NEW"?

Moving forward to the mid-project workshop with Infosys, my team aimed for two goals: go through previous research findings; ideation session on the intersection of finance and wellness.

How to plan this two and a half hours workshop effectively so that our clients, especially those first-meet Infosys team members, can get a sense of the work we did and moving forward? In another words, how to communicate the new? Metaphor is our answer. We used two different subjects to explain financial planning, one is journey, another one is fitness. When conducting the workshop, we separated participants into two groups based on the metaphors.

Finance as a journey

-

Is it better to drive straight through or take breaks? What is the difference between a break and a delay? And what about detours?

-

Mapping- when we know a precise destination, digital tools work well. But what if we just have an intention or a feeling- what if we need a compass, not a map?

Finance as health + fitness

-

What works better- a precise tool (measure heart rate) or a general guideline (break a sweat everyday)?

-

Is there and authority you trust? Perhaps a doctor, a friend or a publication, and when you have questions, what is your next step?

Take a look at our overall workshop plan.

Through this workshop, our clients got involved with the team and the topic. Two metaphors were validated and inspiring ideas were generated to help us think outside the box.

PHASE 6: DESIGN PRINCIPLES

Moving from learning to design, my team took a more macro perspective, integrating our previous research findings with feedback learned from the workshop, which allowed us to create insights that directly drove the design of platforms.

Tiny Habits

To achieve financial wellness, I will need to start some new habits and stop some old ones.

Because habit change is challenging, I want a tool that helps me take small steps that slowly build to big results.

Leveling Up

To achieve financial wellness, I will need to leave behind the subtle pleasure of ignorance and immaturity.

Because leveling up is challenging, I want a tool that helps me see trade-offs and make informed choices.

Right Tools For The Job

To achieve financial wellness, I don't need every metric, chart, and forecast, but I do need some tools to help me navigate.

Because tool selection is challenging, I want a relaxed environment that allows me to experiment with different approaches to find the right one.

Emotions Are Real

To achieve financial wellness, I can't follow advice that urges me to leave emotions out of it.

Because emotions is challenging, I want a tool that supports my ability to both feel my feelings and make sound choices.

Give Me A Hand

To achieve financial wellness, I need suggestions on good paths to pursue and companionship along the way.

Because isolation is challenging, I want a tool that supports my ability to learn from others while gaining confidence in my ability to choose for myself.

Make The Future Feel Concrete

To achieve financial wellness, I need to take actions today that won't have an impact until the future.

Because of future-focus is challenging, I want a tool that maintains momentum on present-actions that will lead to eventual results.

PHASE 7: FINAL CONCEPTS

The design journey we been token on. With a few rounds of ideation, we end up with a pile of idea cards which later on were clustered into 4 final concepts.

Generate Principles

Developed six design principles based on previous learning and feedback from the workshop

Concept Exploration

Brainstormed ideas for concepts following the six design principles

Converge Concepts

Clustered and categorized concepts ideas into different themes

Final Concepts

Consolidated the clusters into four final concepts

CONCEPT 1

Minimum Viable Money is a platform for users with no-to-low financial knowledge to take the first step. Users build healthy financial habits and learn what they need to know to maintain a minimum viable financial wellness in their daily lives.

Precursor

With its promise to Get a Lemonade Policy in 90 Seconds, this insurance company makes it easy for its customers to act on their good intentions. Its playful, pink design and choice architecture support the emotional payoff of completing a dreaded transaction in record time.

Minimum Viable Money is solving...

-

Lower the barrier for everyone to start taking care of their everyday finance

-

Minimize cognitive load to start and continue

Minimum Viable Money's key features include...

-

Retail banking 101--checking, savings, credit, payments

-

Property and life insurance

-

One size fits all (at the beginning)

How does it works?

Isabella describes herself as “math-phobic” and she hates the red-tape and fine-print of interacting with her bank. Although she earns a reasonable wage, she avoids even simple transactions because it’s such a hassle to muster up the necessary vigilance to avoid being taken advantage of or ripped off.

After listening to a friend rave about MVM, she downloaded the app--it managed to make a serious topic feel simple and friendly without being patronizing.

She set up a new savings account labeled Winter Getaway and checked Yes to explore moving her checking account to MVM.

CONCEPT 2

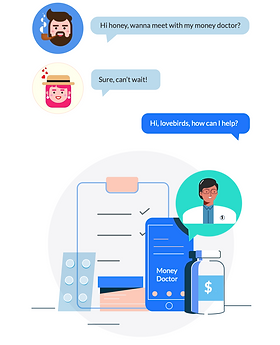

The Money Doctor Is In is a helper who provides holistic examination and diagnosis of user’s financial wellness for those with wages, not yet wealth. Suggests a tailored financial plan with ongoing check-ups.

Precursor

Personal Fitness Trainer

Armed with a clear understanding of a client’s goals and challenges, the Personal Trainer develops a plan and provides accountability for following through, even when following through is difficult. Over time the plan changes to reflect current reality.

-

Blend of real people and AI interfaces

-

Diagnose & provide solutions

-

Blend of rigidity & flexibility

The Money Doctor Is In's key features include...

-

A single point of contact for financial information

-

An expert point-of-view, not just information

-

A safe place to ask naive questions

The Money Doctor Is In is solving...

How does it works?

Noah’s Linkedin shows he’s doing great- two promotions in four years. But his buddies are all buying their first homes, and Noah doesn’t feel ready for what looks like too big of a leap.

It’s been a year since his first money doctor appointment--time for Noah’s annual review. Everything from his investment portfolio to his insurance coverage is considered. “You are a homeowner now, and that comes with some obvious changes,” the money doctor explains, “let’s make sure we catch the non-obvious changes too.”

At Noah’s first appointment, his money doctor explained that first they would review the current state of Noah’s financial life, and they would discuss hopes and concerns for the future.

“People buy property for different reasons,” explained the Money Doctor, giving Noah a property prioritization tool. Noah realized that having a space to barbecue with his friends was at the top of his list.

Noah’s money doctor has some surprising news. “Compared to your cohort, your savings are fantastic. But your earnings aren’t where they could be--in fact, you are in the bottom 20% for your job title in this part of the country. Want some coaching on salary negotiation? ”

Noah introduces his fiancee to the money doctor. “Congratulations! Let’s explore how you two want to structure your financial lives together. We’ll look at some options and then decide whether you want to see me as individuals and as a couple, or if you’d like a referral. Shall we get started?”

CONCEPT 3

Moneyly is a tool for teaching financial terms and methods, and tracking a user’s learning progress as they ask more questions and gain increasing sophistication.

Precursor

Grammarly uses AI to identify grammar, spelling, punctuation, word choice, and style mistakes and suggest context-specific corrections. Grammarly explains the reasoning behind each correction, allowing users to make informed decisions about whether, and how, to correct an issue.

Moneyly is solving...

-

Lack of access to financial knowledge

-

Fear of not asking the right question

-

"I don’t know what I don’t know"

Moneyly's key features include...

-

Layers over existing tools

-

Provides just-in-time guidance, prompts, and recommendations

-

Tracks behavior over time, ranks activity in relation to cohort

How does it works?

Logan thought the job interview was going well, although parts of it were confusing. At one point the HR rep noted that the company had shifted from a defined benefit plan to a defined contribution plan and Logan nodded along even though he had no idea what was being said.

During a break, Logan ran the document through the Moneyly filter and learned that defined benefit meant a pension plan, while defined contribution was a 401(k) retirement savings plan. His recruiter had mentioned that the company offered a pension to its employees, so Logan was disappointed to learn of the change but relieved to fully understand the implications of moving forward.

CONCEPT 4

My Style, My Plan, My People is a digital assessment system enables users to learn about their own financial management style. Then users can build a plan by combining variable modules that work best for them. The users can also follow and learn from peers who share a similar profile with them.

Precursor

By explicitly tailoring their offering to those who feel alienated from mainstream fitness and diet approaches, NerdFitness offers an accessible sense of community along with a suite of free and paid tools learn, change and level up.

My Style, My Plan, My People is solving...

-

A tool for all vs. A tool for my style

-

What my parents did is not working for me; I need a new community of support

My Style, My Plan, My People's key features include...

-

"Money style" self-sorting instrument

-

Suggested peer professionals to follow

-

Suggested activity modules to complete

-

Uses big data from social media to tailor your information

PHASE 8: ROADMAP

To finalize our design offerings, the team spent some time to think through the implementation road map, and for each concept, we listed a key factor based on a timeline.

PHASE 9: EVALUATION

At the last stop of our design journey, we made two sharing out separately with Infosys and Allstates. The overall financial feedbacks were positive and proved that our thinking was right on the spots.

SPECIAL THANKS TO OUR WONDERFUL TEAMMATES

Co-created By Institute of Design Research Team:

Andrew Reynolds, Ariel Chen, Tyler Besecker, Xuning Guo

Guidance By Institute of Design Instructors:

Vijay Kumar

Client: